Thinking, Fast and Slow

In the book Thinking, Fast and Slow, the author, Daniel Kahneman, talks about the experiencing self and remembering self. Kahneman first recalls a study involving patients undergoing a painful colonoscopy, for which at the time of the study there was little anesthetic or other drugs to ease the pain. Every 60 seconds patients were asked to record their pain on a level of zero, indicating no pain, to ten, indicating intolerable pain. The experience for each patient varied considerably, with the shortest lasting 4 minutes and the longest lasting over one hour. These measures based on reports of momentary pain were called hedonimeter totals. Surprisingly, the feedback from the patients was not as anticipated.

The Peak-End Rule and Duration Neglect

Kahneman writes:

When the procedure was over, all participants were asked to rate “the total amount of pain” they had experienced during the procedure. The wording was intended to encourage them to think of the integral of the pain they had reported, reproducing the hedonimeter totals. Surprisingly, the patients did nothing of the kind. The statistical analysis revealed two findings, which illustrate a pattern we have observed in other experiments:

- Peak-end rule: The global retrospective rating was well predicted by the average of the level of pain reported at the worst moment of the experience and at its end.

- Duration neglect: The duration of the procedure had no affect whatsoever on the ratings of total pain.

Experience or Memory?

Kahneman recalled a short anecdote, also alluding to the same phenomenon:

A comment I heard from a member of the audience after a lecture illustrates the difficulty of distinguishing memories from experiences. He told of listening raptly to a long symphony on a disc that was scratched near the end, producing a shocking sound, and he reported that the bad ending “ruined the whole experience.” But the experience was not actually ruined, only the memory of it. They experiencing self had had an experience that was almost entirely good, and the bad end could not undo it, because it had already happened. My questioner had assigned the entire episode a failing grade because it had ended very badly, but that grade effectively ignored 40 minutes of musical bliss. Does the actual experience count for nothing?

As with the medical patients, the retrospective rating was influenced by the peak-end rule. Kahneman notes that mixing up experience with memory is a common cognitive illusion. Here is the problem:

The experience self does not have a voice. The remembering self is sometimes wrong, but it is the one that keeps score and governs what we learn from living, and it is the one that makes decisions. What we learn from the past is to maximize the qualities of our future memories, not necessarily of our future experience. This is the tyranny of the remembering self.

The Cold-Hand Experiment

This idea led Kahneman and his colleagues to design an experiment where participants submerged one hand in painful but not intolerable cold water for a certain length of time. The participants used their free hand to record the amount of pain they were feeling while the experiment occurred. The participants had two trials. For one, a hand was submerged 14° Celsius water for 60 seconds, after which time they removed it and were given a warm towel. The other trial was for 90 seconds, and while the first 60 seconds were identical to the other trial, the last 30 seconds the experimenter released a valve that warmed the water 1°, a noticeable difference which slightly decreased the pain. Then the participants were asked how they wanted the third trial: exactly the same as the first or exactly the same as the second.

The first two trials were very controlled. Half the participants experienced the 60 second trial first and the 90 second trial second, and the other half vice versa in order to prevent the sequence of experience influencing the choice for the third trial. In addition, the experiment was designed to conflict the two selves. The experiencing self obviously had a more painful time during the long trial. If the first 60 seconds are the same, why endure the extra 30, even if they are slightly less painful? However, based on the peak-end rule, the long trial is preferable because the ending wasn’t as painful as the short trial, with the peaks being equal.

What did they participants choose for the third trial?

They choose the long trial. “Fully 80% of the participants who reported that their pain diminished during the final phase of the longer episode opted to repeat it, thereby declaring themselves willing to suffer 30 seconds of needless pain in the anticipated third trial.”

Why the discrepancy?

The remembering self had a more favourable memory of the long trial, despite the duration, due to the peak-end rule. Even though this conflicted with the experiencing self, the remembering self is the one that makes the decisions.

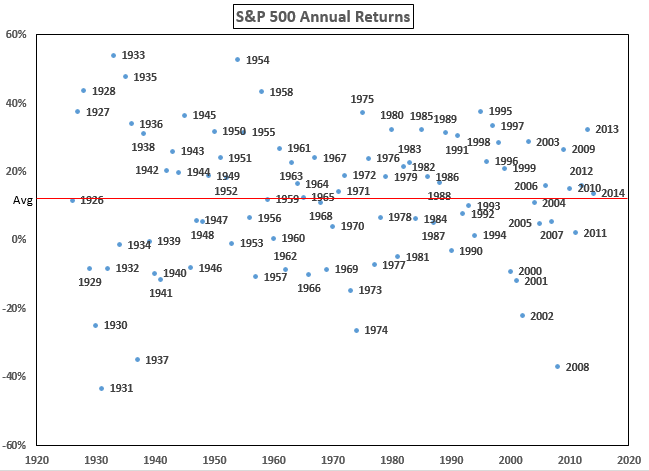

A somewhat recent post from Ben Carlson triggered me to think of how the discrepancies between the experiencing self and remembering self might be present in investing. In Playing the Probabilities, a post he wrote earlier last month, Carlson used this chart: