The most ubiquitous challenge I have faced that I was not aware of during college is what Roger Gibson calls frame-of-reference risk. Essentially, frame-of-reference risk consists of individuals mistakenly comparing their globally diversified portfolios to the S&P 500.

The value of holding a globally diversified portfolio is straightforward for most: in addition to the old adage of “not putting all your eggs in one basket,” it results in a more favorable risk-return tradeoff. However, Roger Gibson suggests that this often increases frame-of-reference risk.

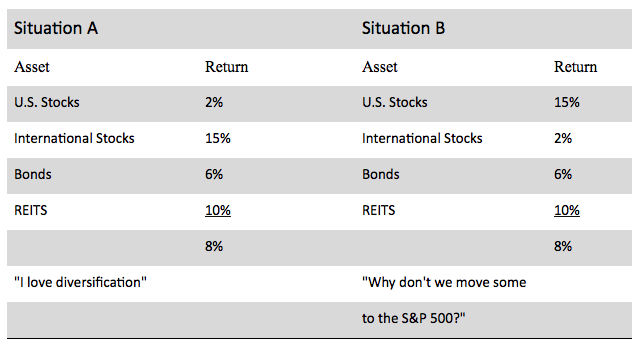

A table best illustrates the problem:

(this is a simplification. assume equal weighting)

In both scenarios the individual is comparing the return of the portfolio (8%) to U.S. Stocks return. In situation A they like what they see. In situation B they do not. (And in fact want to invest more in the best asset - the opposite of what rebalancing calls for.)

Considering the nature of the media in the United States, this is not surprising. Turn on CNBC and it is feast or famine with the Dow Jones Industrial Average and the S&P 500; either the sky is falling or we are all going to be rich. This has been particularly relevant the last several years as the United States stock market has performed well while most other countries have struggled.

Josh Brown wrote a post recently summing up frame-of-reference risk to a tee. Here it is verbatim:

I had dinner last weekend with a financial advisor friend who works on a large wirehouse team based here in New York. Last year “was a major pain in the ass” he told me. He had to remind his clients again and again about the wisdom of global asset allocation while the S&P gained 14% and the rest of the world slumped.

Convincing someone that there is a right way to invest for the long term is hard enough, “re-closing them on our approach every few months is nearly impossible,” he said. I agreed with him. I spent a lot of last year blogging about the frustration among professional wealth managers borne of the huge dispersion between US and foreign stocks. As James Osborne says, what works over most years doesn’t work during every year.

“All the data I could come up with to prove the truth wasn’t enough. People don’t want to see the data when there’s a party going on and they feel left out.”

This year is a different story, he tells me. He got an email the other day from a client to the effect of “Thanks for keeping my portfolio intact and not listening to me when I complained.” Supposedly he had kept the guy from an all-in bet on US stocks just before Christmas. The US stock market is now flat with where it was the first week of Thanksgiving. International stocks have gone berserk to the upside.

So far this year, the power of a global portfolio has reasserted itself, right on schedule – just at the moment where it looked like there was no reason to allocate outside the “best house” ever again:

table via Bank of America Merrill Lynch

The reality is that foreign stocks and US stocks take turns outperforming each other in roughly four year increments. The last such timeframe where foreign developed equities beat the S&P was from 2003 to 2007. There’s no way of seeing the next such streak coming. The first five months of 2015 could be a blip or the start of something bigger.

The point is that it’s likely a diversified portfolio, if history is worth anything at all, will ultimately reward the investors who can stick with it. Even through years like 2014. “They can judge me against the S&P 500 this year if they want,” he said with a laugh.

If you fired your advisor last year to run off and join the Circus of What’s Working Now, don’t be surprised if you find yourself making yet another change in the near future when the grass turns out not to have been greener.

Frame-of-reference risk is basically a simplified version of applying home-country bias to this asset quilt:

via J.P. Morgan Asset Management

When the green box (large cap, represented by the S&P 500) is below the asset allocation box, individuals love diversification. See 2008. When the green box is above the asset allocation box, as it has been the last six years, individuals question the allocation decisions, especially when all you hear from the television shows is “the Dow sets a new high!!”

With diversification, one will never have a portfolio equal to the worst performing asset class, which would have occurred in 2002 if one had held solely the S&P 500; however, one will never have a portfolio equal to the best performing asset class either. While “don’t put all your eggs in one basket” intuitively makes sense, it is easier said than done. When I was coming out of college I erroneously believed diversification was a no-brainer. It certainly is the top strategy in my opinion, but as the advisor in the Josh Brown article stated, “People don’t want to see the data when there’s a party going on and they feel left out.” This is the challenge for advisors: through communication and managing expectations, helping clients avoid improperly benchmarking themselves to their home country’s large cap stocks when they hold a more diversified portfolio.